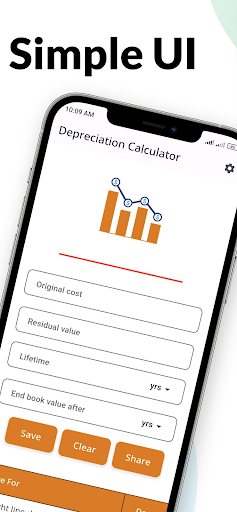

Features Depreciation Calculator

The asset depreciation calculator offers users three distinct methodologies to gauge the rate at which the value of an asset diminishes over time.It empowers you to evaluate the straight-line depreciation model, the declining balance depreciation method, and the sum of years digits depreciation approach.

With these options, you can make informed comparisons and choose the most suitable method for your asset valuation needsThe process of calculating the cost of an asset over its lifespan, known as depreciation in accounting circles, serves as a pivotal method for reallocating the expense of a tangible asset across its useful duration.

To delve deeper into this concept, lets examine the following scenario:Upon acquiring a significant tangible asset, such as machinery or a vehicle, a company incurs a substantial expenditure that could wield a pronounced impact on its annual income statement.

To mitigate the abrupt fluctuations in the income statement, attributable to the acquisition of costly assets, accounting practices advocate for the smoothing of such expenses in the companys financial records.

This is achieved by dispersing the cost of the asset over its useful lifespan, where only a fraction of its value is recognized as current expenses each year.

By adopting this method, the company is able to evenly distribute the expenses over the entirety of the assets operational lifespan, thereby fostering financial stability and clarity in its reporting mechanisms.In practice, various methods exist for calculating depreciation, based on either the passage of time or the degree of asset usage.

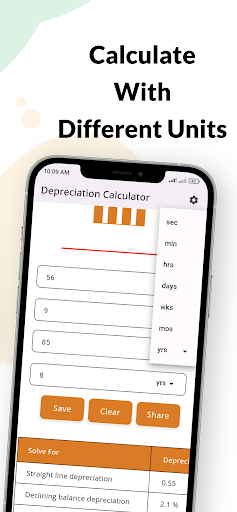

These methods are applicable to different types of tangible assets:Straight-line Depreciation: A method where the same amount of depreciation is deducted from the assets value each year over its useful life.Declining Balance Method: A method where depreciation is calculated as a fixed percentage of the remaining book value of the asset each year.Double Declining Balance Method: Similar to the declining balance method, but with double the rate of depreciation.Annuity Depreciation: A method where the depreciation expense remains constant each period.Sum-of-Years-Digits Method: A method that accelerates depreciation by summing the digits of an assets useful life.Units-of-Production Depreciation Method: Depreciation is based on the actual usage or production of the asset.Units of Time Depreciation: Depreciation is calculated based on the time an asset is used.Group Depreciation Method: Assets within a group are depreciated together, considering the total value of the group.Composite Depreciation Method: A combination of different depreciation methods applied to various components of an asset.Its important to note that regardless of the method used, the total depreciation over an assets lifespan remains the same.

Only the timing of depreciation varies among methods.Next, well focus on the three most common depreciation methods: straight-line, declining balance, and sum of years digits, detailing their formulas and calculation processes.Residual Value and DepreciationThe residual value (or salvage value) represents the estimated worth of an asset after its intended useful life.

While this value is an approximation, it serves as a crucial factor in accounting.

When selling an asset, any difference between the sale price and the net book value (original cost minus accumulated depreciation) results in a gain or loss.For an asset used until the end of its expected life, the residual value is typically zero.

Productivity Tools

Boost your productivity with powerful tools and features.

Learning Tools

Enhance your learning experience with interactive features.

Lifestyle

Enhance your lifestyle with personalized tips and features.

See the Depreciation Calculator in Action

Get the App Today

Available for Android 8.0 and above